When the Strait of Hormuz closes, who feeds the city?

The case for resilient food infrastructure in an age of geopolitical disruption

The conflict in the Middle East is, first of all, a human tragedy. Thousands of people killed, millions displaced, a region in crisis. But alongside that immediate toll, a quieter emergency is taking shape, one that will reach dinner tables far beyond the conflict zone.

Since late February 2026, the Strait of Hormuz has been effectively blockaded, sending global energy markets into their worst disruption since the 1970s oil crisis. The waterway between Iran and Oman, just 21 nautical miles at its narrowest, carries roughly 20 million barrels of oil per day, representing about 20% of global petroleum liquids consumption. It also handles around 20% of global LNG trade, with no viable alternative maritime route for producers like Qatar. UN and ESCAP estimates put the oil price rise at around 45% and gas at 55% since late February, with fertilizer prices up 35%. The downstream effects on food are already measurable. Urea, the world's most widely used nitrogen fertilizer, has surged more than 25% in price since the end of February. Qatar has halted production at its largest urea manufacturing facility. Agricultural cargoes are stranded or rerouting across the Persian Gulf.

The American Farm Bureau Federation wrote directly to the US President, warning of 'a threat to our food security'.

Sources: U.S. Energy Information Administration (EIA), 2025; UN News / ESCAP, March 2026.

Why food systems are exposed

Contemporary food supply chains depend on three assumptions: open shipping lanes, stable input prices, and accessible energy. The Hormuz blockade has removed all three simultaneously.

The strait is not only a critical artery for oil and gas. It is the primary transit route for the fertilizers upon which global crop production depends. Qatar, Saudi Arabia, Oman, and Iran collectively account for a major share of globally traded urea and phosphates, and nearly all of it passes through Hormuz. UNCTAD estimates the strait handles roughly one-third of global seaborne fertilizer trade, around 16 million tonnes per year.

IFPRI has documented that higher energy and input costs risk reigniting food price inflation in countries where retail prices had only recently stabilised. The exposure is not evenly distributed. In Sub-Saharan Africa, over 90% of fertilizer is imported, and food expenditure already accounts for a large share of household income. South and Southeast Asian economies dependent on Gulf inputs are registering renewed inflationary pressure. The World Economic Forum has assessed the fallout as reshaping global commodity markets, food systems, and financial conditions, potentially for years.

“The question is not whether disruption will come. It is whether the systems feeding our cities are built to absorb it.”

A structural response, not a short-term fix

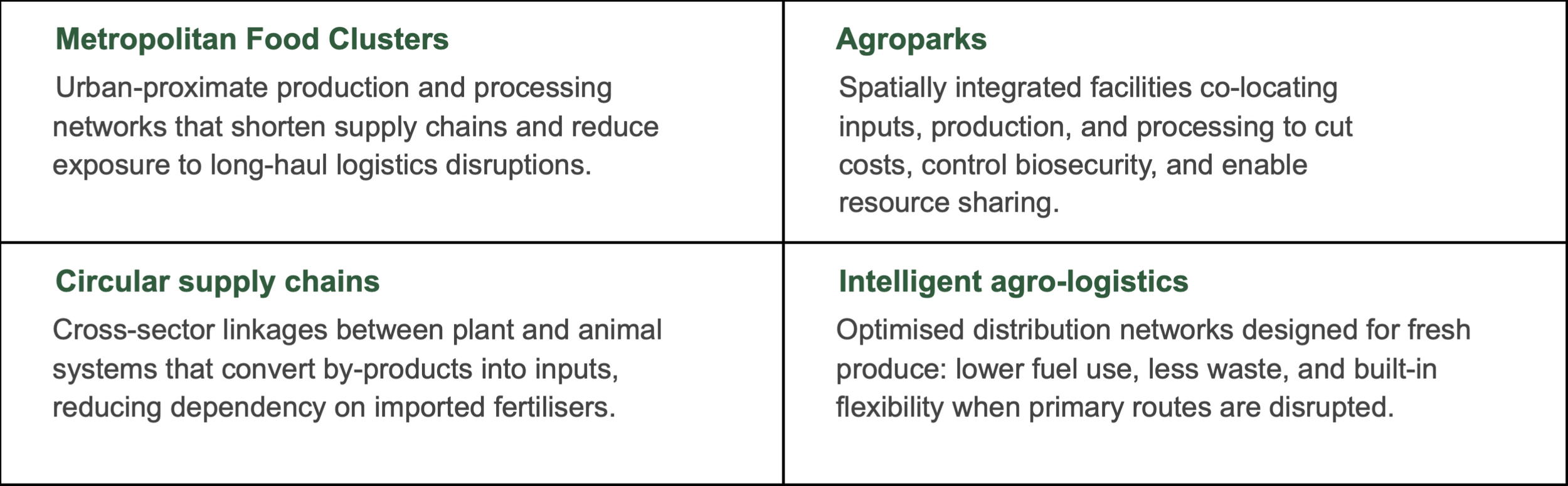

WMFC was established to address exactly this structural weakness in how cities are fed. Rooted in agri-food systems research at Wageningen University and Research, our work centres on one core finding: food systems that cluster production, processing, and distribution closer to urban demand are measurably shorter, more circular, and more resistant to long-chain disruptions.

This is not a retreat to local self-sufficiency. It is a redesign of food system architecture based on evidence. WMFC works with investors, governments, and entrepreneurs to plan and develop Metropolitan Food

Clusters and Agroparks: spatially integrated facilities that bring together inputs, production, processing, and distribution to reduce transport costs, biosecurity exposure, and dependency on volatile commodity chains.

The case for investment now

Research consistently shows that food system vulnerability is a function of design, not geography or luck.

Systems built around long, energy-intensive chains with few redundancies fail predictably under geopolitical stress. Systems designed around shorter chains, regional clustering, and circular flows do not.

For policymakers, this crisis makes the link between food security and national resilience planning impossible to ignore. UN ESCAP has called for longer-term efforts to diversify trade routes and supply chains as a policy priority. Metropolitan Food Clusters operationalize exactly that: reducing the number of chokepoints a city's food supply depends on, and building redundancy into the system before the next shock, not after.

For investors and developers, the fundamentals are clear. Urban food demand is growing. Geopolitical risk in long supply chains is not declining. Infrastructure that positions production and processing closer to consumption centres is increasingly valuable, both commercially and strategically. WMFC provides the

planning, analytical, and co-design capacity to translate that opportunity into operational projects, across continents and at scale.

“Food system resilience is an infrastructure problem. It requires investment decisions, not just policy statements.”

The human dimension

We write this with full awareness of what is happening to people across the region. The food security implications are not separate from that suffering. Food insecurity and conflict are mutually reinforcing: one deepens the other.

Fertilizer price increases of 40 to 60% lead farmers, particularly smallholders, to reduce application rates.

Yield losses follow six to twelve months later. For populations already at nutritional risk heading into late 2026, that lag is the most dangerous part of this crisis.

Food systems built around shorter chains, regional production, and circular resource flows are more equitable as well as more resilient. They reduce the distance between production decisions and the people who depend on them. That is the work WMFC was built to do.

WMFC works with governments, investors, and developers on the planning and realisation of Metropolitan Food Clusters and Agroparks. If you are considering an investment in food system infrastructure, we would welcome the conversation.

References

1. Wikipedia. (2026). 2026 Strait of Hormuz crisis. Retrieved March 23, 2026, from

https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

2. U.S. Energy Information Administration. (2025, June). Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint. https://www.eia.gov/todayinenergy/detail.php?id=65504

3. U.S. Energy Information Administration. (2025). About one-fifth of global liquefied natural gas trade flows through the Strait of Hormuz. https://www.eia.gov/todayinenergy/detail.php?id=65584

4. UN News / ESCAP. (2026, March 20). Middle East war shockwaves ripple through Asia-Pacific fuel and supply chains. https://news.un.org/en/story/2026/03/1167167

5. Food Navigator USA. (2026, March 12). Food prices rise as Middle East tensions hit energy and fertilizer costs. https://www.foodnavigator-usa.com/Article/2026/03/12/food-prices-rise-as-middle-east-tensions-hit-energy-and-fertilizer-costs/ 6. Food Navigator USA, ibid. Citing Qatar fertilizer production halt, March 2026.

7. Food Navigator USA, ibid. Citing American Farm Bureau Federation letter to President Trump, March 2026. 8. CNN Business. (2026, March 5). Surging energy prices and threats to shipping: how the Middle East war could hurt the global economy. https://www.cnn.com/2026/03/05/economy/economy-impact-middle-east-war-intl

9. Cordiant Capital. (2026). Middle East Conflict and Food Inflation Through the Fertilizer Channel. Citing UNCTAD (2026, March 10). Strait of Hormuz disruptions: implications for global trade and development. https://www.cordiantcap.com/middle-east-conflict-and-food -inflation-through-the-fertilizer-channel-financial-risk-management-considerations/

Wageningen Metropolitan Food Clusters · wmfc.nl Page 3 of 4

10. CNBC. (2026, March 12). A global food price shock looms as Middle East war continues. Quoting International Food Policy Research Institute (IFPRI). https://www.cnbc.com/2026/03/12/iran-war-food-prices-fertilizer-hormuz-countries-impacted-.html 11. CNBC, ibid. Citing University of Texas at Austin data on Sub-Saharan Africa fertilizer import dependency. 12. TIME. (2026, March 16). How the war with Iran is impacting economies in Asia.

13. World Economic Forum. (2026, March). The global price tag of war in the Middle East.

https://www.weforum.org/stories/2026/03/the-global-price-tag-of-war-in-the-middle-east/

14. Wageningen MFC. (n.d.). Design and planning of Agroparks and Metropolitan Food Clusters.

https://www.wmfc.nl/english-1/our-offer/design-planning/

15. Biovision / IPES-Food. (2021). Money Flows: What is Holding Back Investment in Agroecological Research for Africa? See also: WUR. (2022). Metropolitan food clusters and urban food system resilience. Wageningen University and Research. 16. UN News / ESCAP, op. cit.

17. Wageningen MFC. (n.d.). Investors. https://www.wmfc.nl/investors

18. World Hunger Education Service. (2026, March). Fertilizer prices and hunger increase from Middle East war. https://www.worldhunger.org/fertilizer_prices/